The so called ‘Great Aussie Dream’ is to own your own home right? The banks want you to take out a 30 year loan and take all of those 30 yrs paying it off and along the way, paying them handsomely. Then why are so many couples and families struggling to meet their own repayments when interest rates are at an all time low? Is the Great Aussie Dream a fallacy and is there another way?

The Australian Dream or Great Australian Dream is a belief that in Australia, home-ownership can lead to a better life and is an expression of success and security.

If this is so, why are so many mortgage owners ending up broke or on the pension by the time they reach retirement (age 65).

The number of mortgage owners that are now under ‘mortgage stress’ is increasing dramatically by the day. We are in a period of extremely low interest rates, our unemployment rate across the nation is stable, yet most Australians are spending more than they earn and taking all of 30 yrs to pay down their bad debt on their own home to then downsize to a smaller dwelling in retirement and attempt to live off the difference.

This my friends is a ‘flawed plan’.

Australians are not retiring comfortable at 65 and most still have to continue working beyond 65 because their downsizing and super balances are not enough to see them live another 20 yrs with mid 80’s being the average lifetime age of males and females in Australia at present.

Martin North from the Digital Finance Analytics says below –

Mortgage stress is a poorly defined term. The RBA tends to equate stress with defaults (which remain at low levels on an international basis). A wider definition is 30% of income going on mortgage repayments (not consistently pre-or post tax). This stems from the guidelines of affordability some banks used in 1980’s and 1990’s, when economic conditions were different from today. This is a blunt instrument. DFA does not think there is a good indicator of mortgage stress, so we use a series of questions to diagnose mortgage stress focusing on owner occupied households. Through these questions we identify two levels of stress – Mild and Severe.

- Mild = households maintaining repayments, but by reprioritizing expenditure, borrowing more on loans or cards, and refinancing

- Severe = households who are behind with their repayments, are trying to sell, are trying to refinance, or who are being foreclosed

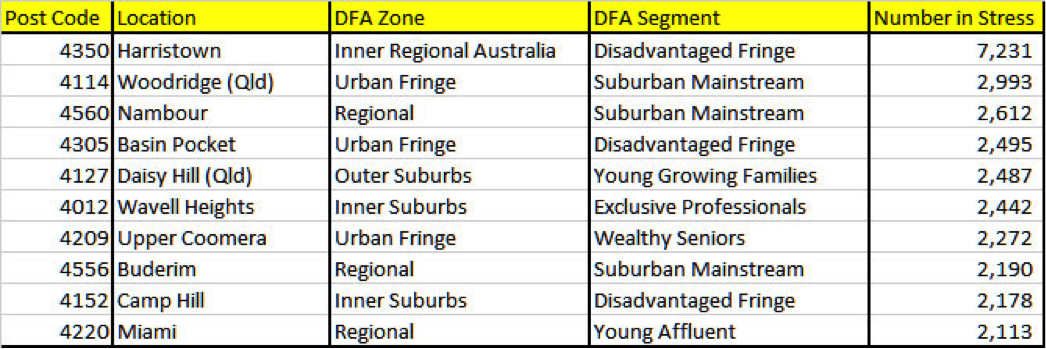

Here is a list of the top 10 across QLD. Depending on the location, the predominate segment varies quite considerably. Harristown, 4350 a suburb of Toowoomba is located to the southwest of the city centre and has the highest count of stressed households across Australia.

Now whilst DFA have only analysed QLD in this survey, it shows the severity of this issue in a cross section of suburbs that are both regional and city based.

So how can we avoid this happening to us –

- Understand and monitor your own cashflow in your family

- Avoid bad debt in your life and before buying your own home, you have 3 mths of personal buffers to cover costs in the event of loss of income, sickness etc

- Your insurances are up to date and relevant including Life, Trauma, TPD and Income Protection.

- Do not live beyond your means eg. Paying for a holiday on credit card and then taking the next 3 yrs to pay if off.

- Start investing early and educate your kids to do the same

- Invest in residential real estate that are in quality towns or cities and will continue to perform long term for you in retirement

- Rent in an area that you want to live in and build up a sizable deposit before committing to 30 yrs of bad debt

- Structure your finances and your investments so that you do not take 30 yrs to pay down your debt. Eg. We have helped clients do this in less than 10 yrs and still enjoy the lifestyle that they want.

For a personalised analysis of your own situation and a look to see what is possible for you right now, simply click on the link below and come and chat to us.

Happy Investing